In a conventional portfolio, bonds provide income and reduce volatility relative to equities. In a Sharia-compliant portfolio, conventional bonds are not an option — they pay interest (riba), which is prohibited in Islamic law. Sukuk are the Islamic finance alternative: instruments that provide regular income from asset ownership or commercial arrangements, not from lending money at a fixed rate.

Why conventional bonds are not Sharia-compliant

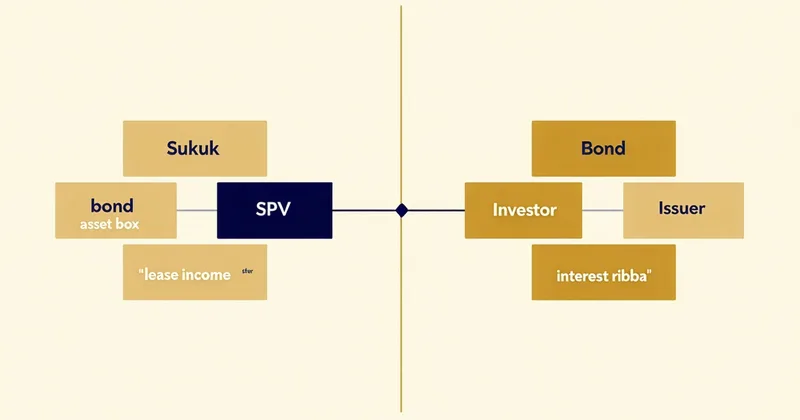

A conventional bond is a loan. The issuer (government or corporation) borrows money from investors and promises to pay a fixed rate of interest plus return the principal at maturity. The interest payment is riba — a predetermined, time-based return on money lent, which Islamic jurisprudence prohibits because it separates financial gain from productive economic activity and creates an asymmetric obligation between lender and borrower.

This is why a conventional Stocks & Shares ISA with a 60/40 equity-bond allocation cannot simply be replicated for a halal investor. The 40% bond allocation needs a different instrument entirely.

What Sukuk are

Sukuk (singular: Sak) are certificates that represent proportional ownership in an underlying asset, project, or commercial arrangement. Rather than paying interest for the use of money, Sukuk pay a return derived from the performance of the underlying asset — a lease payment, a profit-sharing arrangement, or proceeds from a trade transaction.

The key Sharia principle at work is that money must be deployed in productive activity, and returns must be tied to that activity rather than to the passage of time. If the underlying asset performs well, Sukuk holders benefit. If it underperforms, they share in that risk — which is why certain Sukuk structures that attempt to guarantee capital return are regarded as problematic by some scholars.

The main Sukuk structures

Ijarah (lease-based) Sukuk are the most common structure used by sovereign and corporate issuers. The issuer sells an asset to a special purpose vehicle (SPV), which then leases it back. Sukuk holders receive periodic lease payments. At maturity, the asset is repurchased. The UK government has issued sovereign Sukuk using Ijarah structures — the first in 2014, followed by subsequent issuances. Ijarah Sukuk are widely accepted across madhabs as Sharia-compliant.

Murabaha (cost-plus-sale) Sukuk involve the purchase and immediate resale of a commodity at a pre-agreed profit margin. The buyer (issuer) agrees to pay the purchase price plus a markup over time. Returns are fixed and known in advance — the profit margin, not an interest rate. Murabaha structures are common in corporate Sukuk and money market instruments.

Musharakah (partnership) Sukuk represent participation in a joint venture. Returns are variable, based on the venture's profits. Some scholars prefer Musharakah Sukuk because the profit-sharing structure most closely reflects the Islamic finance ideal of partnership over debt. However, Musharakah Sukuk with guaranteed capital return are considered problematic by AAOIFI and many scholars.

Risks specific to Sukuk

Sukuk carry risks that differ from conventional bonds in important ways. First, liquidity risk: the secondary market for Sukuk is less developed than for conventional bonds, particularly for corporate issuances. Selling before maturity may be difficult or may result in an unfavourable price. Second, asset risk: because Sukuk are tied to an underlying asset, the asset's condition and legal ownership structure matter — these require due diligence that does not apply to conventional bonds. Third, Sharia risk: a subsequent ruling from a scholar or supervisory board might determine that a particular structure is not compliant, affecting market confidence in the issuance.

How Wealth8 uses Sukuk

Wealth8 holds Ijarah and Murabaha Sukuk in the fixed-income allocation of Sharia-compliant portfolios. Musharakah Sukuk with guaranteed capital return are excluded by the Sharia Supervisory Board. The Board reviews Sukuk holdings quarterly alongside equity holdings, applying the same AAOIFI-aligned framework. Sukuk that drift out of compliance — because the underlying structure changes or a new scholarly opinion is issued — are flagged for review and removal.

Sukuk sit within your Wealth8 ISA alongside Sharia-screened equities and riba-free cash equivalents. The tax-free wrapper applies to Sukuk income as it does to equity dividends — no income tax on distributions, no Capital Gains Tax on any appreciation in value.

This article is for informational purposes only and does not constitute personal financial or investment advice. Capital at risk. The value of your investments can fall as well as rise. Sharia compliance is reviewed by Wealth8's independent Sharia Supervisory Board; compliance does not guarantee investment returns.